The Bottom Of The Market Feels Like A Bumpy Road

It’s the New Year, and just in time the banks are raising interest rates, but just a little – so far. However, the banks are also relaxing their down-payment requirements because they are seeing increased confidence in the housing market. The truth, according to one banker friend I spoke with is because they are not making any money. They need to make loans to make money. In some markets borrowers can now borrow 95% of a property’s value. Of course one would hope this means property values are not going down any further and loan applicants are going to be scrupulously vetted?

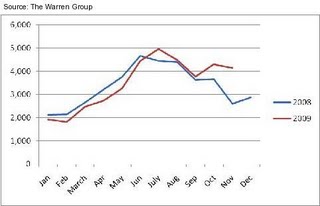

Despite favorable sales figures as we finished out this year, Tim Warren Jr., CEO of the Warren Group sees home prices bouncing up and down along the bottom during the next 3-6 months, and possibly throughout most of 2010 even though sales figures will appear to continue trending positively. This is the way it was in the early 90’s as we pulled out of the last recession. Some economists call this an “L” recession. For sure the recovery is going to be slow, but I do think it is safe to say we are at the bottom albeit a bumpy bottom. I believe in making a decision about when is the best time for you to buy an investment property one indicator you should pay attention to is interest rates. When interest rates go up this can herald the onset of an inflationary period.

Warren feels it was the rush to take advantage of the initial first-time home buyer tax credit by signing contracts before November 2009 expiration that contributed the biggest boost to the market. Wednesday’s WSJ reported that first-time buyers made up 51% of purchases in November, according to NAR. The initial first-time home buyer tax credit has been extended and broadened to include more potential buyers which may once again give a boost to the housing market. Contracts have to be signed by April 30, 2010 with closing dates on or before June 30, 2010. According to Carl Reichardt, an analyst with Wells Fargo, “The spring selling season would be critical to determining whether a possible double-dip is at hand, or whether housing’s recovery will regain steam.”

Tim Warren believes another reason for the upturn is the brighter unemployment figures in Massachusetts which in turn enhance consumer confidence. Okay, but one of my sources tells me the actual national unemployment figure is above 17%, if you factor in the non-registered ‘shadow’ unemployed.

News Flash: Massachusetts unemployment rate drops slightly from 8.9% to 8.8%

Read about it here > http://www.businessconnector.biz/news/show/523

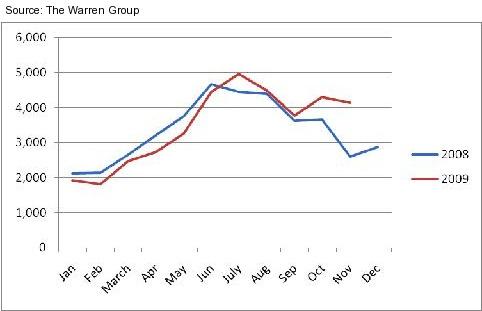

Despite favorable sales figures as we finished out this year, Tim Warren Jr., CEO of the Warren Group sees home prices bouncing up and down along the bottom during the next 3-6 months, and possibly throughout most of 2010 even though sales figures will appear to continue trending positively. This is the way it was in the early 90’s as we pulled out of the last recession. Some economists call this an “L” recession. For sure the recovery is going to be slow, but I do think it is safe to say we are at the bottom albeit a bumpy bottom. I believe in making a decision about when is the best time for you to buy an investment property one indicator you should pay attention to is interest rates. When interest rates go up this can herald the onset of an inflationary period.

Warren feels it was the rush to take advantage of the initial first-time home buyer tax credit by signing contracts before November 2009 expiration that contributed the biggest boost to the market. Wednesday’s WSJ reported that first-time buyers made up 51% of purchases in November, according to NAR. The initial first-time home buyer tax credit has been extended and broadened to include more potential buyers which may once again give a boost to the housing market. Contracts have to be signed by April 30, 2010 with closing dates on or before June 30, 2010. According to Carl Reichardt, an analyst with Wells Fargo, “The spring selling season would be critical to determining whether a possible double-dip is at hand, or whether housing’s recovery will regain steam.”

Tim Warren believes another reason for the upturn is the brighter unemployment figures in Massachusetts which in turn enhance consumer confidence. Okay, but one of my sources tells me the actual national unemployment figure is above 17%, if you factor in the non-registered ‘shadow’ unemployed.

News Flash: Massachusetts unemployment rate drops slightly from 8.9% to 8.8%

Read about it here > http://www.businessconnector.biz/news/show/523

In January, it is predicted that 1,000,000 unemployed workers will lose their benefits. Another prediction is going to be a surge in commercial foreclosures as more companies lay off workers and close doors in leased office spaces. But who knows? I still believe in miracles.

Labels: 1031 Tax Deferred Exchange, EXCLUSIVE Buyer Agency, Luxury Real Estate, Martha's Vineyard Real Estate, mortgage rates, Peter Fyler, Resort and Second-Home, SplitRock Real Estate, Tax Credit

posted by Peter C. Fyler, SplitRock Real Estate LLC at 3:49 PM

0 comments

![]()